Structured Products

.png)

.png)

The term “structured product” can seem intimidating and overly complex, but it is not as complicated as it may initially appear.

Consider a scenario where a novice investor is given two options:

Most investors would likely choose the first option because of its familiarity, viewing the structured product as a “black box”. However, if the choice was re-phrased as, “Would you like to buy shares of Apple directly, or would you prefer an investment option that customizes your risk and return in a way that better matches your needs?” the perception changes. This highlights that a structured product is essentially a customized investment. Using the term “customized investment” is more approachable and accurately describes the product.

A structured product is an investment tailored to an investor’s specific needs, including the choice of the underlying asset, maximum acceptable loss, and investment duration.

Banks initially created structured products to lower their funding costs. Instead of issuing standard coupon-paying bonds, they issued notes with an embedded option linked to an underlying asset’s performance. The bank would use the proceeds like a regular bond but would invest a portion in an option for the investors instead of paying a conventional coupon.

This was advantageous for both parties:

Early structured products were often simple “zero plus call” structures, which included:

These components create a note that protects the principal while offering upside participation if the asset appreciates.

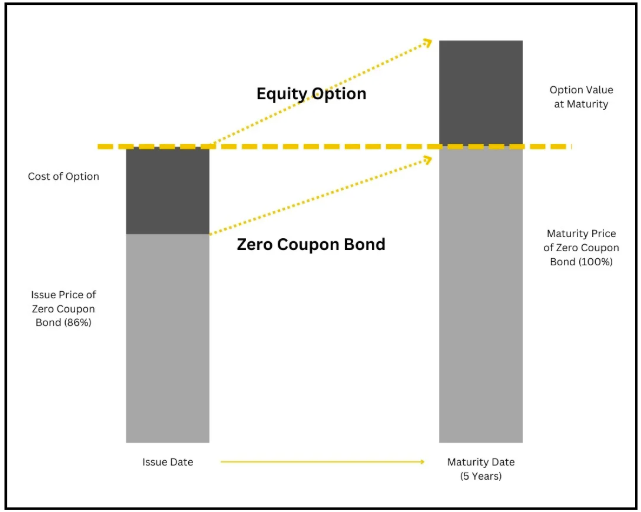

If a bank can raise five-year funds at about 3 % per annum, its total interest cost over that period would be around 15 %. This means the present value of the bank’s five-year zero-coupon bond is about 85 % of its face value. A five-year call option on an equity index might cost around 14 % of the notional value.

The bank can bundle the zero-coupon bond (~85 %) with the 14 % call option. Instead of a 3 % annual coupon, it offers investors participation in the index’s upside over five years with principal protection. This was appealing to many investors as they got the full upside if the index rose and capital protection if it performed poorly.

This structure, also known as a capital-protected note, has two main parts:

Structured notes evolved from a cost-reduction tool for banks into a new profit center. Today, nearly every major global bank has a structured products desk as a key part of its derivatives operations. While some funding benefits remain, revenue is now mainly generated by marking up the value of the packaged investment. Investors gain capital protection and the potential for market-linked returns.

The world of structured products is vast and highly customizable. It is more important to understand the payoff structure and risk profile than the marketing name. Before investing, one should ask:

A Reverse Convertible pays a guaranteed coupon and returns 100 % of the principal at maturity, provided the underlying asset does not fall below a specified barrier.

Example Setup

The coupon is guaranteed regardless of the underlying’s performance. Profitability depends on the underlying’s price at maturity. The full principal is returned as long as the underlying has not declined by more than 30 %.

Potential Risks

If the underlying asset drops significantly (more than 30 %), the principal is at risk. For example, if Apple finishes at 60 % of its initial price, the investor would only recover 60 % of their capital.

Investor Profile Checklist

This product exchanges some potential upside for a fixed coupon and partial protection.

An Autocallable product is similar to a reverse convertible but includes a feature for early termination if certain conditions are met on observation dates. It pays a coupon and provides principal protection as long as the underlying does not breach a barrier. If the underlying is trading above its initial level on a specified date, the product redeems early. Otherwise, it continues to the next observation date.

Example Setup

Return Scenarios

The coupon is guaranteed. Profitability depends on the underlying’s price, and the principal is recovered if the price has not declined by more than 30 %.

Potential Risks

If the underlying declines by more than 30 %, the investment is at risk. For example, if it ends at 60 % of its initial value, the investor recoups only 60 % of the invested capital.

Checklist for Investor Profile

This product is suitable for those prepared to exchange uncertain stock upside for a steadier income stream and partial downside protection.

Participation notes are growth-oriented products that allow investors to share in the underlying asset’s performance, unlike income-focused structures. Instead of coupons, the investor gains from the asset’s upside.

A gain is realized if the underlying’s share price is higher at maturity, with the amount depending on the level of appreciation.

The main risk is a significant drop in the underlying’s price (e.g., more than 20 %). For instance, if the asset ends at 70 % of its starting value, the investor would recover only 70 % of their investment.

Checklist for Investor Profile

This structure allows for keeping upside potential while enjoying some protection against moderate declines.

.png)

.png)

.png)

Fintech banking advanced technology to offer agile, user friendly & services to traditional banking.